If this was asked at this point last year, the response would be in major contrast as to the biggest risks threatening businesses this year and beyond. Risk from a pandemic was perhaps a tiny inclusion on a business insurance policy, not given much thought from one year to the next and why should it when nothing on this scale had been seen since the early 1900s. Now a year into lockdowns and with talk of a third wave coming, COVID-19 and the host of related risks it brought with it, are not yet done causing disruption in a globalized economy that wasn’t ready for it.

COVID and related risks still dominate

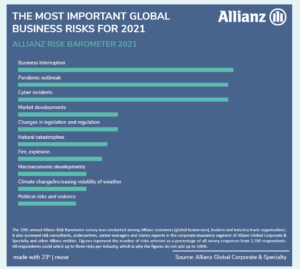

We were all optimistic that 2021 would mark the end of a situation that defined risk for business, but sadly there are multiple business interruption factors still in play and present ongoing threats for as long as the pandemic persists. The initial interruptions to global production and supply chain remain number one risks to business given the level of uncertainty as to when we might see an easing of local and international restrictions. A global annual survey undertaken by Allianz shared the top three future risks to business as business interruption, pandemic outbreak and cyber incidents, with pandemic risk moving up from position 17 to position 2 since the last survey.

All of these top three risks are inextricably linked, either caused by or a consequence of the pandemic. The potential to suffer damage from cyber-attacks, data breaches and other types of cyber crime increases as organizations progress with digitalization of business models and prepare in some cases, for a fully remote workforce.

Although these risks will remain top-of-mind through 2021, other risks haven’t simply gone away, they’ve been temporarily overshadowed.

Market changes and growth

Consumer spending will only rebound once confidence returns and that is largely dependent on the successful roll-out of an effective vaccine. When that confidence does return, we can expect a spike in spending driven by a world eager to start living again. It may or may not be a short-lived rebound, but there is definite opportunity for those companies and start-ups that have already innovated and shown flexibility in the face of adversity, to be able to take advantage of any upturn. Likewise, businesses should also prepare for a potential downturn to avoid too much exposure to the risk of dwindling revenues, not an easy task unless you can put cash aside for a rainy day.

Disruptive tech start-ups recognized permanent changes in consumer behavior and accelerated change that was slow to happen in traditional industries. Longer term, for businesses that fail to adapt, the risks are amplified. In manufacturing for example, businesses will need to adopt automation technologies or be less able to handle future disruptions and find themselves too reliant on human labor.

MacroEconomic policies

Global debt from emergency government spending will reach its highest levels post-COVID. Withdrawing of stimulus too early can result in a slower recovery time for the economy, something that we saw after the 2008 financial crisis in the US when focus was put on reducing the deficit, arguably too early. The last thing businesses need as they’re just getting back onto their feet is for the rug to be pulled from under them which is precisely what could happen if governments decide to reign in spending and increase interest rates.

Small and large businesses alike could also be impacted by the unwillingness of global economies to trade internationally. Policies to source more product from the domestic market and reduce free trade is a big factor in whether or not a business is able to scale-up.

In the US, the high concentration of technology and telecom companies with complex global supply chains, meant that more businesses reported ‘severe’ disruption to supply and a report by Euler Hermes suggests that 62% will be looking to source new suppliers in the longer-term and about a quarter of businesses would prefer to find ‘home’ suppliers. These kinds of changing allegiances need consideration as part of the wider risk mitigation strategy.

Insolvency and consolidation

For the most part, insolvencies have remained stable or actually dropped up to now. The risk of insolvency increases at such time as the federal aid dries up and spending in the economy declines. Monitoring cash flow closely to improve the cycle of cash coming in against cash going out can help to mitigate insolvency risk.

Mergers and acquisitions in the US declined by 50% in the first half of 2020 as any plans for expansion were put on hold to address more pressing in-house issues. Lack of interest from buyers could prevent a business from generating the capital they need through the sale of underperforming locations or assets. Conversely, a business consolidating in a period of constrained cash flow might well find it wasn’t the right move, in as much as it hampers their ability to expand their reach and take on new opportunities.

Climate change

Climate change has been a rising threat to business for many years and one which wasn’t altered by the pandemic. Whilst businesses dealt with the immediate risk of failure, extreme weather events including wildfires, flooding and heat waves posed a very real threat worldwide and continue to do so as we’ve witnessed already this month with the unprecedented storms unfolding in Texas.

Business losses from climate change seem to be increasing in severity and cost and should be high on the radar of companies wanting to mitigate future risk, particularly those that rely heavily on single production plants and equipment.

A multi-faceted approach to future risk

Without touching on any potential political and legislative changes, these are just a handful of the risks that businesses will need to contend with in the years to come. There is no one activity that can eliminate risk entirely and actually businesses have always been able to operate with some level of risk so long as there is a clear strategy.

In a situation that remains fluid, businesses will need to take into account a wider range of extreme risks than previous; not only COVID-related but the ones that preceded. Building a comprehensive mitigation strategy that covers both immediate and longer-term threats will be crucial for a business to prosper.

Whilst some businesses have so far endured the challenging conditions of COVID-19, adapting to a ‘new normal’, others closed as they couldn’t sustain heavy blows to revenue and uncertainties of the supply chain and still make their day-to-day financial commitments.

Most economic risk can be counteracted with a business model that allows operation with minimal overheads, saving as much money as possible for the maintenance of steady cash flow when times are hard. Towards the end of 2021 going into next year, it may become harder to maintain a good cash flow situation because of the risks we’ve discussed. If you’re at all concerned about the shape of your business currently, it might be time to look at the options to improve your working capital before lending gets even tighter.

Reach out to us to discuss any concerns you might have about your working capital needs and how we might be able to work together for the success of your business.

Canadian Business and The 2022 Federal Budget – Key Takeaways

It’s fair to say small businesses didn’t feature massively in the Canadian 2022 Federal Budget proposed last week. Although there…

Read More

Ultimate Year End Review for Business Owners

We’ve reached the final few weeks of 2022 and whether December is a busy time or a quieter period for…

Read More

American Business Women’s Day

Sallyport Commercial Finance Celebrates American Business Women’s Day

View Now

Popkoffs Client Testimonial

Popkoffs Client Testimonial

View Now